Running a business in Victoria is a unique grind. Between navigating the unpredictable weather, managing the rising cost of supplies, and trying to stand out in a hyper-competitive market, the last thing you want to do is spend your weekends buried in receipts. But when it comes to keeping more of your hard-earned revenue, finding a proactive Tax accountant for small business Melbourne isn’t just a compliance exercise—it’s a massive competitive advantage.

Whether you’re pouring lattes in a Brunswick cafe, running a digital agency out of Richmond, or managing a fleet of tradies across the south-eastern suburbs, the financial landscape has shifted dramatically in 2026. The ATO is watching closer than ever, but they’ve also confirmed some permanent concessions that can save you tens of thousands if you know how to apply them. Let’s break down exactly what you need to know this financial year, how the latest federal budgets impact your bottom line, and exactly how to keep more cash in your pocket.

Why Melbourne Businesses Face Unique Tax Hurdles

Let’s be real for a second: running a business down here means dealing with a specific set of rules that interstate businesses don’t always face. It’s not just about federal income tax; it’s the state-level obligations that often catch founders off guard.

If your team is growing, you’re suddenly going to hit the State Revenue Office’s (SRO) radar. In Victoria, once your total annual wages hit the $1.0 million threshold, you are on the hook for a 4.85% payroll tax. Add in WorkCover premiums, the newly implemented Payday Super rules starting July 1, 2026, and managing cash flow through our distinct seasonal lulls, and it becomes pretty obvious why a generic, once-a-year tax agent won’t cut it. You need someone who understands the local ecosystem, anticipates your state tax liabilities, and structures your operations so you aren’t hit with a massive, unexpected bill in May.

2026 Australian Small Business Tax Rates Explained

Understanding your baseline tax rate is the foundation of any good financial strategy. Federal tax brackets and company rates have seen crucial updates that affect how you should draw income from your business.

If your business operates as a company, the government has maintained the highly beneficial 25% tax rate for “base rate entities”. To qualify for this reduced rate (down from the standard 30%), your aggregated turnover must be under $50 million, and no more than 80% of your revenue can come from passive sources like rent, royalties, or interest.

For sole traders, partnerships, and trust beneficiaries, your business income flows through to your personal tax return and is taxed at individual marginal rates. The great news for the 2026-2027 financial year is the continuation of tax relief. From July 1, 2026, the tax rate for income between $18,201 and $45,000 drops from 16% to 15%, which provides an immediate boost to your take-home pay.

The Permanent $20,000 Instant Asset Write-Off

For years, business owners have played a guessing game with the federal budget, waiting to see if equipment deductions would be extended. Finally, the 2026 Federal Budget has provided certainty: the $20,000 instant asset write-off is a permanent fixture for small businesses with an aggregated turnover of less than $10 million.

This is a game-changer for your growth strategy. It means you can immediately deduct the full business-use portion of eligible assets—like a new commercial oven, specialized trade tools, or office technology—provided each individual asset costs less than $20,000 and is installed ready for use. You don’t have to deal with complex depreciation schedules over several years. Because the threshold applies per asset, if you buy four separate items at $15,000 each, you can instantly write off all of them, massively reducing your taxable income for the year.

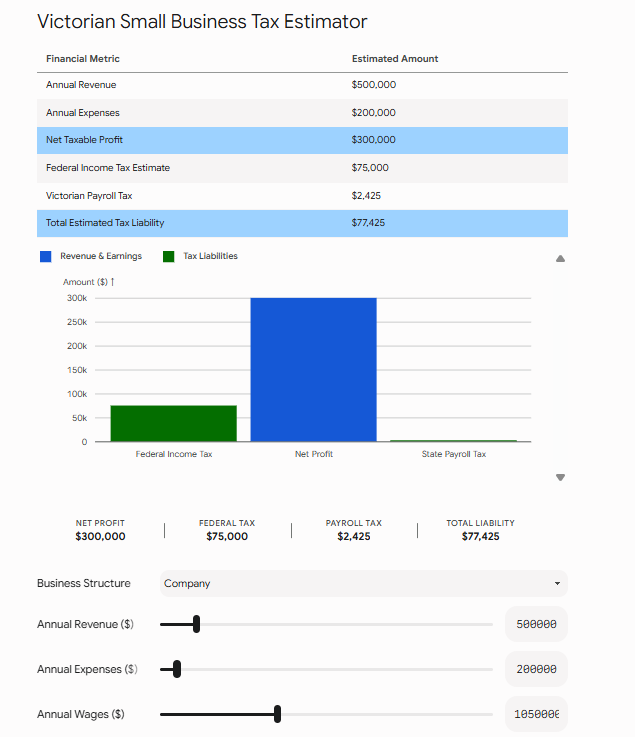

See the Numbers: Victorian Small Business Tax Estimator

Understanding your liability requires crunching the numbers. Use this interactive estimator to see how your business structure and revenue impact your overall federal and state tax burden.

Key insight: Hitting the $1,000,000 wage threshold in Victoria triggers payroll tax on every dollar above that mark. Factoring this into your hiring roadmap is critical to avoiding cash flow crises.

5 Proven Strategies to Boost Your Cash Flow

A great accountant doesn’t just lodge your BAS; they actively look for legal avenues to keep money in your business. Here are five top-tier strategies relevant for 2026:

-

Switch to GST Cash Accounting: If your aggregated turnover is under $10 million, you are eligible to account for GST on a cash basis. This means you only pay the ATO the GST when your client actually pays you, rather than when you issue the invoice. This simple switch can save a growing business from severe cash flow bottlenecks.

-

Prepay Allowable Expenses: Bring forward deductible expenses before June 30. Prepaying up to 12 months of insurance premiums, commercial rent, or software subscriptions immediately reduces this year’s taxable income.

-

Master the 70-Cent WFH Rule: The ATO’s fixed-rate method for working from home is 70 cents per hour. This rate covers electricity, internet, and phone usage without the headache of calculating complex apportionments for every utility bill.

-

Prepare for Payday Super: From July 1, 2026, employers must pay superannuation at the same time as wages, abandoning the old quarterly system. With the Super Guarantee rate permanently fixed at 12%, transitioning your payroll software now will prevent compliance penalties later.

-

Utilise Simplified Depreciation Pools: For assets that exceed the $20,000 write-off limit, eligible businesses can pool them together. This allows you to claim a 15% deduction in the first year and a 30% deduction each subsequent year, greatly simplifying your record-keeping.

Federal vs. Victorian State Taxes: A Quick Reference

Navigating the split between federal obligations (ATO) and state obligations (SRO) is where most small businesses trip up. Keep this quick-reference table handy.

| Tax Type | Authority | 2026 Rate & Key Rule |

| Company Income Tax | Federal (ATO) | 25% for base rate entities under $50m turnover. 30% otherwise. |

| Individual Income Tax | Federal (ATO) | Progressive rates. 15% applies from $18,201 to $45,000 (from July 2026). |

| Superannuation Guarantee | Federal (ATO) | 12% of ordinary time earnings, paid on payday from 1 July 2026. |

| Payroll Tax | State (VIC SRO) | 4.85% on annual wages exceeding the $1.0 million threshold. |

| GST | Federal (ATO) | 10% on most goods/services. Cash accounting available under $10m. |

How to Choose the Right Accountant in Melbourne

Finding the right advisor is about matching their expertise to your growth stage. You want to move away from a “transactional” tax agent and find a “strategic” partner.

Look for someone with a CPA or CA qualification who is a Registered Tax Agent. Ask them directly about their experience with Victorian state taxes, specifically payroll tax structuring and WorkCover. A high-quality accountant will want to review your business structure (whether you should be a Sole Trader, Company, or Family Trust) to ensure you are maximizing asset protection and legally minimizing your tax footprint. Finally, prioritize a professional who implements cloud-based forecasting tools—your accountant should be looking at the dashboard through the windshield with you, not just analyzing the rear-view mirror once a year.

Conclusion

The 2026 financial landscape offers massive opportunities for Melbourne small businesses that are organized, compliant, and strategic. From the permanent $20,000 instant asset write-off to the shifting individual tax brackets, the rules are designed to help you reinvest in your growth. However, the introduction of Payday Super and strict SRO audits means the margin for error is shrinking. Partnering with a specialized local accountant is the single highest-ROI decision you can make for your business this year.

Frequently Asked Questions

What is the small business company tax rate in 2026?

The company tax rate is 25% for “base rate entities.” To qualify, your business must have an aggregated turnover of less than $50 million, and 80% or less of your assessable income can come from passive sources.

At what point do I have to pay payroll tax in Victoria?

In Victoria, you must register and pay payroll tax when your total Australian wages exceed the annual threshold of $1.0 million. The current rate is 4.85%.

Is the instant asset write-off still available?

Yes. As of the 2026-27 Federal Budget, the $20,000 instant asset write-off has been made permanent for eligible small businesses with an aggregated turnover of less than $10 million.

What are the Payday Super rules?

Starting 1 July 2026, employers are legally required to pay their employees’ superannuation at the same time they pay their wages (e.g., weekly or fortnightly), rather than on a quarterly basis. The rate remains at 12%.