Running a business in Australia is hard work. You are constantly juggling clients, managing cash flow, and trying to keep your head above water. The absolute last thing you need is a freak accident, a break-in, or a legal dispute threatening to wipe out everything you have built. That is why getting the right cover is non-negotiable. But let’s be honest, reading through product disclosure statements is nobody’s idea of a good time. If you want to compare business insurance Australia, you have to look past the flashy marketing and figure out exactly what you are paying for.

In this comprehensive guide, I am going to walk you through the reality of business insurance. We will cover what policies you actually need, what exclusions to watch out for, how to match your cover to your specific industry, and how to make sure you are not overpaying for your premium.

Why You Need to Compare Business Insurance in Australia

Every dollar counts when you run your own operation. It is incredibly tempting to just grab the cheapest policy you find online, tick a box, and forget about it until renewal time. However, treating insurance as just another administrative chore is a massive gamble.

Being underinsured can destroy a business overnight. In fact, insurance gaps cost small businesses an average of $1.4 million in 2022. When you compare policies, you are not just looking for a cheaper monthly payment; you are looking for the exact coverage limits and inclusions that match your daily operational risks. A policy that works perfectly for a freelance graphic designer working from a laptop in Sydney will be completely useless for a commercial plumber operating a fleet of vehicles in Brisbane. Taking the time to properly compare options ensures you are paying for protection that will actually respond when a crisis hits, rather than leaving you stranded with a denied claim.

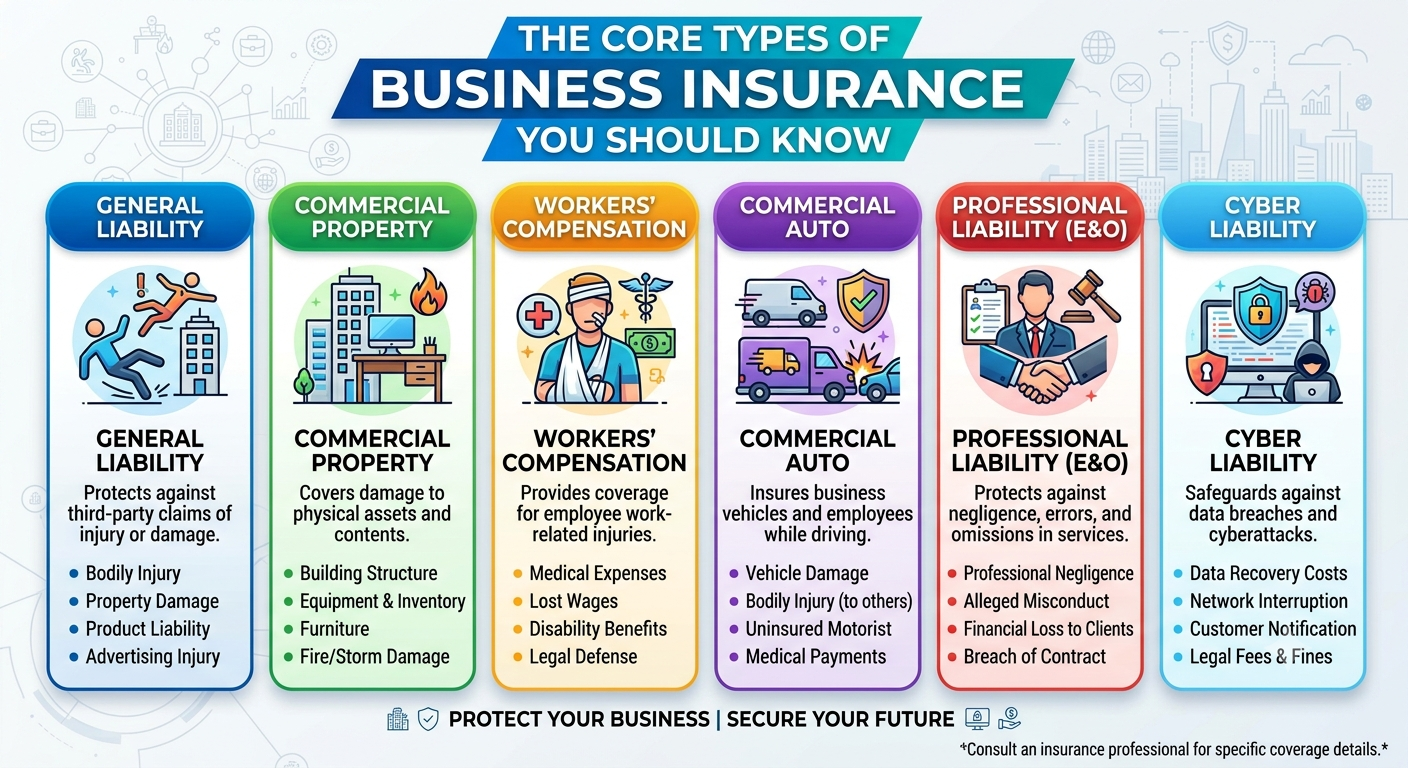

The Core Types of Business Insurance You Should Know

Before you start looking at quotes, you need to understand the building blocks of commercial insurance. Most providers will allow you to bundle several of these into a single “Business Pack,” but knowing what each element does is critical.

1. Public Liability Insurance

If your business interacts with the physical world in any way—whether clients visit your office, you visit their homes, or you sell a physical product—you need public liability cover. This policy steps in if a third party is injured or their property is damaged as a result of your daily operations.

For example, if a customer slips on a wet floor in your shop, or you accidentally knock over an expensive vase while working in a client’s living room, this cover pays for the legal defence costs and any court-awarded damages. The stakes are high; average trip-and-fall claims for Australian retailers hover around $35,000. Many event organisers, local councils, and landlords will actually demand proof of public liability (usually a minimum of $10 million or $20 million in cover) before they will do business with you.

2. Professional Indemnity Insurance

While public liability covers physical accidents, professional indemnity (PI) covers financial damage caused by your professional advice or services. If you charge a fee for your expertise—such as an accountant, architect, IT consultant, or real estate agent—you are exposed to claims of negligence, errors, or omissions.

If a client alleges that your bad advice, a software bug in your code, or a miscalculation in your design cost them money, PI insurance covers your legal defence and any subsequent settlements. For certain professions, such as tax agents, migration agents, and allied health practitioners, holding PI insurance is a strict regulatory requirement.

3. Workers Compensation Insurance

If you employ staff in Australia, workers compensation is not optional; it is a strict legal requirement. This insurance pays for lost wages, medical expenses, and rehabilitation costs if a staff member becomes ill or is injured because of their work.

Because it is a statutory requirement, it is regulated heavily at the state and territory level. For example, you will deal with the State Insurance Regulatory Authority (SIRA) in New South Wales, WorkSafe in Victoria, and WorkCover in Queensland.

4. Cyber Liability Insurance

Cybercrime is no longer just a problem for massive corporations. Small and medium enterprises are heavily targeted because they often have weaker digital security. If your business collects customer data, processes online payments, or uses cloud storage, cyber insurance is highly recommended.

This policy helps cover the costs associated with data breaches, ransomware attacks, and business email compromise. The risk is severe, with data being stolen in roughly 86% of all ransomware incidents. A good policy will help cover the costs of IT forensics, notifying affected customers, and recovering lost data.

5. Business Interruption Insurance

Also known as business continuation insurance, this cover replaces your lost income if your business is forced to close or scale back operations due to an insured event (like a fire, major storm, or severe vandalism). It helps you keep the lights on, pay your ongoing fixed costs (like rent and supplier contracts), and pay your staff while you rebuild and get back on your feet.

Industry-Specific Insurance: What Fits Your Trade?

General policies are a great starting point, but every industry has unique risks. When you compare business insurance in Australia, you need to look for industry-specific additions:

-

Trades and Construction: Tradies need specific cover for their physical assets. “Tools of trade” insurance protects portable work gear from theft and damage. Construction businesses also heavily rely on contract works insurance to cover projects while they are actively being built.

-

Retail and Hospitality: Cafes, restaurants, and retail shops need to protect their physical premises. This includes glass cover (for broken shopfronts), theft insurance, and food contamination cover to protect against stock spoilage if the power goes out.

-

Health and Wellness: Allied health professionals (like physiotherapists, chiropractors, and aged care workers) require specialised medical malpractice insurance to protect against claims arising from patient treatment.

-

Transport and Logistics: If you move goods, you need commercial motor and fleet insurance to cover vehicle damage, alongside marine cargo insurance (which covers goods in transit by road, rail, air, or sea).

How Much Does Business Insurance Cost in Australia?

There is no flat rate for business insurance. Insurers calculate your premium based on your specific risk profile. Understanding how they view your business can help you negotiate better rates and avoid nasty surprises at renewal time.

Here is a breakdown of the core factors that drive the cost of your premiums:

| Pricing Factor | How It Affects Your Premium |

| Industry Risk | High-risk physical trades (like roofing or tree removal) pay significantly more for liability than office-based consultants. |

| Annual Turnover | Higher revenue means higher stakes. Insurers view larger financial volumes as an increased risk for larger claims. |

| Business Location | Operating in areas prone to natural disasters (floods, cyclones) or high crime rates will drastically increase property cover costs. |

| Staff Headcount | More employees directly increase the cost of mandatory workers compensation and general liability exposures. |

| Claims History | A clean history keeps premiums low. Frequent past claims will flag you as high-risk, driving up renewal prices. |

Tip for saving money: Many insurers offer premium discounts if you can prove you actively manage your risks. Installing security systems, keeping detailed incident logs, and training staff on safety protocols can all help lower your costs.

Top Insurance Providers and Brokers in the Australian Market

The Australian market is highly competitive, featuring a mix of direct insurers, underwriting agencies, and specialist broker platforms.

When looking at direct providers, heavyweights like Allianz, QBE, CGU, Chubb, AAMI, and GIO dominate the landscape. These providers offer massive capacity and highly customisable business packs. For example, QBE was recently recognised as the Large General Insurer of the Year for 2025, and providers like Allianz and CGU consistently perform well regarding claim acceptance rates.

However, many business owners prefer to use broker platforms and comparison services to shop the market efficiently. Platforms like BizCover, Choosi, and Ausure allow you to input your business details once and receive comparable quotes from multiple leading insurers,,. Using a broker or comparison site can save you hours of reading and ensures you are getting a policy tailored to your specific occupation.

Common Exclusions: What Isn’t Covered?

One of the biggest mistakes business owners make is assuming their policy covers absolutely everything. Insurance is designed to cover sudden, unforeseen accidents—not inevitable wear and tear or intentional bad behavior.

Common exclusions across most business policies include:

-

Deliberate Acts and Fraud: You cannot claim for damages resulting from illegal activities, intentional negligence, or fraudulent behavior.

-

Known Prior Circumstances: If you knew a client was preparing to sue you before you took out a professional indemnity policy, the insurer will not cover that specific claim.

-

Wear and Tear: Property insurance does not cover the gradual breakdown of equipment or building degradation over time.

-

Unlisted Perils: Many policies exclude flood damage unless you specifically request and pay to have it added to your cover.

Always read the Product Disclosure Statement (PDS) to understand exactly what your insurer will refuse to pay for.

The Step-by-Step Guide to Getting the Best Quote

Securing the right insurance shouldn’t be a guessing game. Follow this process to ensure you get the right cover at the best price:

-

Assess Your Risks: Sit down and identify exactly what could cause a severe financial loss to your business. Look at your physical assets, your digital footprint, and your daily interactions with the public.

-

Consult Your Accountant: Before approaching brokers, get professional guidance from your accountant regarding your revenue projections and asset valuations so you insure for the correct amounts.

-

Check Contractual Requirements: Review your commercial lease, client contracts, and industry licenses. Make sure your new policy meets the exact minimum coverage limits required by these agreements.

-

Compare the Market: Use comparison platforms or speak to a dedicated business insurance broker to pull quotes from multiple underwriters. Do not just look at the price—compare the excess amounts and the specific inclusions. Keep in mind that 44% of all complaints reported by insurance brokers in 2022 were regarding small business or farm insurance products, highlighting the importance of checking the fine print.

-

Review Annually: Your business changes every year, and your insurance needs to change with it. Make it a habit to reassess your cover levels every 12 months.

Conclusion

Protecting your livelihood is one of the most important responsibilities you have as a business owner. When you compare business insurance in Australia, you are investing in peace of mind and financial stability. By understanding the core covers like public liability, professional indemnity, and workers compensation, and matching them to your specific industry risks, you can build a safety net that actually works. Take the time to assess your risks, speak to the experts, and review your policies annually. A little bit of due diligence today can save your entire business tomorrow.